Got an opportunity recently to hear about the connectivity progress, challenges and issues in Africa. Agree that Africa is a very large continent with many different countries in different stages of development but it was nevertheless interesting to look at a high level picture on the progress of connectivity in the continent. The presentation by iDate Digiworld is embedded below.

During the mobile world congress, I was pleasantly surprised to see how LoRa ecosystem keeps getting larger. There was also an upbeat mood within the LoRa vendor community as it keeps winning one battle after another. Here is my short take on the technology with an unbiased lens.

It’s seems LoRa is quietly getting some traction, particularly when it comes to industrial / vertical markets. #MWC18pic.twitter.com/KQ6G7JjTU9

To start with, lets look at this short report by Tom Rebbeck from Analysys Mason. The PDF can be downloaded after registering from here.

As can be seen, all major IoT technologies (LoRa, NB-IoT, Sigfox & LTE-M) gained ground in 2017. Most of the LoRa and all of Sigfox networks are actually not deployed by the mobile operators. From the article:

These points lead to a final observation about network deployments – many operators are launching multiple technologies. Of the 26 operators with publicly-announced interest in LTE-M networks, 20 also have plans for other networks; • 14 will combine it with NB-IoT • four will offer LTE-M and LoRa and • two, Softbank and Swisscom, are working with LoRa, LTE-M and NB-IoT. We are not aware of operators also owning Sigfox networks, though some, such as Telefónica, are selling connectivity provided by a Sigfox network operator. The incremental cost of upgrading from NB-IoT or LTE-M to both technologies is relatively small. Most estimates put the additional cost at less than an additional 20% – and sometimes considerably less. For many operators, the question will be which technology to prioritise, and when to launch, rather than which to choose. The reasons for launching multiple networks appear to be tactical as much as strategic. Some operators firmly believe that the different technologies will match different use cases – for example, LoRa may be better suited to stationary, low bandwidth devices like smart meters, while LTE-M, could meet the needs of devices that need mobility, higher bandwidth and support for voice, for example a personal health monitor with an emergency call button. But, a fundamental motive for offering multiple networks is to hedge investments. While they may not admit it publicly, operators do not know which technology will gain the most traction. They do not want to lose significant, lucrative contracts because they have backed the wrong technology. Deploying both LTE-M and NB-IoT – or LoRa – adds little cost and yet provides a hedge against this risk. For operators launching LoRa, there has been the added benefit of being early to market and gaining experience of what developers want and need from LPWA networks. This experience should help them when other technologies are deployed at scale.

The following is from MWC 2018 summary by ABI Research: LPWA network technologies continue to gather momentum with adoption from a growing ecosystem of communications service providers (CSPs), original equipment manufacturers (OEMs) and IoT solution providers. LPWA networks are central to the connectivity offerings from telcos with support for NB-IoT, LTE-M, LoRaWAN, and SIGFOX. Telefonica highlighted SIGFOX as an important network technology along with NB-IoT and Cat M in its IoT connectivity platform. Similarly, Orange and SK Telecom emphasized on their continued support for LoRaWAN along with Cat M in France and South Korea. On the other hand, Vodafone and Deutsche Telekom, while aggressively pursuing deployment of NB-IoT networks, currently have mostly large scale POCs on their networks. ... Smart meters — Utilities are demanding that meter OEMs and technology solution providers deliver product design life of at least 15 years for battery operated smart water and gas meters. LPWA technologies, such as NB-IoT, LoRaWAN, SIGFOX and wireless M-bus, that are optimized for very low-power consumption and available at low cost are clearly emerging as the most favored LPWA solutions.

So someone recently asked me is LoRa is the new WiMax? The answer is obviously a big NO. Just look at the LoRa alliance members in the picture above. Its a whole ecosystem with different players having different interests, working on a different part of the ecosystem.

NB-IoT & LTE-M will gain ground in the coming years but there will always be a place for other LPWA technologies like LoRa.

Finally, here is a slide deck (embedded below) that I really like. The picture above very nicely illustrates that LoRaWAN and Cellular complement each other well. Maybe that is the reason that Orange is a big supporter of LoRa.

So for operators who are just starting their IoT journey or smaller operators who are unsure of the IoT potential, may want to start their journey with LoRa to play around and understand the business cases, etc. In the meantime LTE-M and NB-IoT ecosystem will mature with prices coming down further and battery time improving. That may be the right time to decide on the way forward.

SMS is 25 years old. The first SMS, "Merry Christmas" was sent on 3rd December 1992 from PC to the Orbitel 901 handset (picture above), which was only able to receive SMS but not send it. Sky news has an interview with Neil Papworth - the man who sent the very first one back in 1992 here.

While SMS use has been declining over some time, thanks to messaging apps on smartphones like WhatsApp, Viber, Facebook messenger, etc., it is still thought to be used for sending 20 billion messages per day.

While I dont have the latest figures, according to analyst Benedict Evans, WhatsApp and WeChat combined are now at over 100bn messages per day.

The global SMS system peaked at maybe 20bn messages a day. WhatsApp and WeChat combined are now at over 100bn

According to Daily Mirror, by the end of 2017, researchers expect 32 trillion messages to be sent annually over apps compared to only 7.89 trillion text messages.

You DO understand that everybody in the light blue part can be reached by SMS?

And the green line is all who can be reached by the internet.

FB is far less than green line.

Apps far less than FB.

Whatsapp far less than apps

RT @gasseepic.twitter.com/2ZCZR6ynjI

Tomi Ahonen makes an interesting in the tweet above, all cellular phone users have SMS capability by default while only smartphone users who have downloaded the messaging apps can be reached by a particular messaging app. The reach of SMS will always be more than any competing apps.

That is the reason why GSMA is still betting on RCS, an evolution of SMS to compete with the messaging apps. My old post on RCS will provide some basic info here. A very recent RCS case studies document from GSMA here also provides some good info.

RCS will have a lot of hurdles and challenges to overcome to succeed. There is a small chance it can succeed but this will require change of mindset by operators, especially billing models for it to succeed.

Dean Bubley from Disruptive Analysis is a far bigger skeptic of RCS and has written various posts on why it will fail. One such post that makes interesting reading is here.

"Ovum

now forecasts that there will be 111 million 5G mobile broadband

subscriptions at end-2021, up more than fourfold from Ovum’s previous

forecast of 25 million 5G subscriptions at end-2021"

"1

Billion Users of 5G by 2023, with More Than Half in China",

"broadly similar path to 4G LTE technology...more than one in every five

mobile connections."

If we just look at 2025/2026, the estimates vary from 500 million to 2.6 billion. I guess we will have to wait and see which of these figures comes true.

I wrote a post earlier titled '4G / LTE by stealth'. Here I talked about the operators who still had 3G networks while most people had 4G phones. The day the operator switched on the 4G network, suddenly all these users were considered to be on 4G, even if they didn't have 4G coverage just yet.

I have a few questions about what 5G features are necessary for the initial rollout and when can an operator claim they have 5G? In fact I asked this question on twitter and I got some interesting answers.

Question: How many 5G sites does an operator have to deploy so that they can say they have 5G?

Just having a few 5G NR (new radio) sites enough for an operator to claim that they have deployed 5G? Would all the handsets with 5G compatibility then be considered to be on 5G? What features would be required in the initial rollouts? In case of LTE, operators initially only had Carrier Aggregation deployed, which was enough to claim they supported LTE-A. Would 100MHz bandwidth support be enough as initial 5G feature?

Every few years I add Mary Meeker's Internet Trends slides on the blog. Interested people can refer to 2011 and 2014 slide pack to see how world has changed.

One of the initial slide highlights that the number of smartphones are reached nearly 3 billion by end of 2016. If we looked at this excellent recent post by Tomi Ahonen, there were 3.2 billion smartphones at the end of Q1 2017. Here is a bit of extract from that. SMARTPHONE INSTALLED BASE AT END OF MARCH 2017 BY OPERATING SYSTEM

Rank . OS Platform . . . . Units . . . . Market share Was Q4 2016 1 . . . . All Android . . . . . . . . . . . . 2,584 M . . . 81 % . . . . . . ( 79 %) a . . . . . . Pure Android/Play . . . . 1,757 M . . . 55% b . . . . . . Forked Anroid/AOSP . . . 827 M . . . 26% 2 . . . . iOS . . . . . . . . . . . . . . . . . . 603 M . . . 19 % . . . . . . ( 19 %) Others . . . . . . . . . . . . . . . . . . . . . . 24 M . . . . 1 % . . . . . . ( 1 %) TOTAL Installed Base . 3,211 M smartphones (ie 3.2 Billion) in use at end of Q1, 2017

Source: TomiAhonen Consulting Analysis 25 May 2017, based on manufacturer and industry data BIGGEST SMARTPHONE MANUFACTURERS BY UNIT SALES IN Q1 2017

This year, the number of slides have gone up to 355 and there are some interesting sections like China Internet, India Internet, Healthcare, Interactive games, etc. The presentation is embedded below and can be downloaded from slideshare

I am sure that by now everyone is aware of Facebook's attempt to connect the people in rural and remote areas. Back in March they published the State of Connectivity report highlighting that there are still over 4 billion people that are unconnected.

The chart above is very interesting and shows that there are still people who use 2G to access Facebook. Personally, I am not sure if these charts take Wi-Fi into account or not.

In my earlier post in the Small Cells blog, I have made a case for using Small Cells as the best solution for rural & remote coverage. There are a variety of options for power including wind turbines, solar power and even the old fashioned diesel/petrol generators. The main challenge is sometimes the backhaul. To solve this issue Facebook has been working on its drones as a means of providing the backhaul connectivity.

Recently Facebook held its first Telco Infra Project (TIP) Summit in California. The intention was to bring the diverse set of members (over 300 as I write this post) in a room, discuss ideas and ongoing projects.

There were quite a few interesting talks (videos available here). I have embedded the slides and the talk by SK Telecom below but before I that I was to highlight the important point made by AMN.

As can be seen in the picture above, technology is just one of the challenges in providing rural and remote connectivity. There are other challenges that have to be considered too.

Embedded below is the talk provided by Dr. Alex Jinsung Choi, CTO, SK Telecom and TIP Chairman and the slides follow that.

This post contains summary of three interesting events that took place recently.

CW (Cambridge Wireless) organised a couple of debates on 5G as can be seen from the topics above. Below is the summary video and twitter discussion summary/story.

Back in 2011, I was right in predicting that we will not see VoLTE as early as everyone had predicted. Looking through my twitter archive, I would say I was about right.

As I said earlier, CSFB for now and VoLTE around 2014 - RT @mitchellkp: LTE won't find voice anytime soon http://t.co/mn0EwAw

The big issue with VoLTE has always been the complexity. In a post last year I provided a quote from China Mobile group vice-president Mr.Liu Aili, "VoLTE network deployment is the one of the most difficult project ever, the implementation complexity and workload is unparalleled in history".

From a recent information published by IHS, there will only be 310 million subscribers by end of 2016 and 2020 is when 1 billion subscribers can make use of VoLTE. I think the number will probably be much higher as we will have VoLTE by stealth.

Below are couple of case studies, one from SK Telecom, presented by Chloe(Go-Eun) Lee and other from Henry Wong, CTO Mobile Engineering, Hong Kong Telecom (HKT). Hope you find them informative and useful.

In the good old days when people used to have 2G phones, they were expensive but all people cared about is Voice & SMS.

The initial 3G phones were bulky/heavy with small battery life, not many apps and expensive. There was not much temptation to go and buy one of these, unless it was heavily subsidised by someone. Naturally it took a while before 3G adoption became common. In the meantime, people had to go out of their way to get a 3G phone.

With 4G, it was a different story. Once LTE was ready, the high end phones started adding 4G in their phones by default. What it meant was that if the operator enabled them to use 4G, these devices started using 4G rather than 3G. Other lower end devices soon followed suit. Nowadays, unless you are looking for a real cheap smartphone, your device will have basic LTE support, maybe not advanced featured like carrier aggregation.

The tweets below do not surprise me at all:

Another data point for Turkey #4.5G: There were 5 million new LTE subscriber additions on the first *day* of launch. (no 4G before)

Occasionally people show charts like these (just using this as a reference but not pin pointing anyone) to justify the 5G growth trajectory with 4G in mind. It will all depend on what 5G will mean, how the devices look like, what data models are on offer, what the device prices are like, etc.

I think its just too early to predict if there will be a 5G by stealth.

Smartphones have replaced so many of our gadgets. The picture above is a witness to how all the gadgets have now been replaced by smartphones. To some extent hardware requirements have been transferred to software requirements (Apps). But the smartphones does a lot more than just hardware to software translation.

Most youngsters no longer have bookshelves or the encyclopedia collections. eBooks and Wikipedia have replaced them. We no longer need sticky notes and physical calendars, there are Apps for them.

Back in 2014, Benedict Evans posted his "Mobile is Eating the world" presentation. His presentation has received over 700K views. I know its not as much as Justin Bieber's songs views but its still a lot in the tech world. He has recently updated his presentation (embedded below) and its now called "Mobile ate the world".

We sometimes think of the shift to mobile as finished, or almost finished. It isn't. pic.twitter.com/l5gaiMlaoU

Quite rightly, the job is not done yet. There is still long way to go. The fact that this tweet has over 600 retweets is a witness to this fact. Here are some of the slides that I really liked (and links reltaed to them - opens in a new window).

While we can see how Smartphones are getting ever more popular and how other gadgets that its replacing is suffering, I know people who own a smartphone for everything except voice call and have a feature phone for voice calls. Other people (including myself) rely on OTT for calls as its guaranteed better quality most of the time (at least indoors).

Smartphones have already replaced a lot of gadgets and other day to day necessities but the fact is that it can do a lot more. Payments is one such thing. The fact that I still carry a physical wallet means that the environment around me hasn't transformed enough for it to be made redundant. If I look in my wallet, I have some cash, a credit and debit card, driving license, some store loyalty cards and my business cards. There is no reason why all of these cannot be digital and/or virtual.

A connected drone can be considered as smartphone that flies.

The Smartphones today are more than just hardware/software. They are a complete ecosystem. We can argue if only 2 options for OSs is good or bad. From developers point of view, two is just about right.

Another very important point to remember that smartphones enable different platforms.

Old: all software expands until it includes messaging

New: all messaging expands until it includes software

There are some reports that have been recently published on connectivity and connection numbers. This post intends to provide this info.

Facebook released "State of connectivity 2015" report. As can be seen in the picture above, at the end of 2015, estimates showed that 3.2 billion people were online. This increase (up from 3 billion in 2014) is partly attributed to more affordable data and rising global incomes in 2014. Over the past 10 years, connectivity increased by approximately 200 to 300 million people per year. While this is positive news in terms of growth, it also means that globally, 4.1 billion people were still not internet users in 2015. The four key barriers to internet access include: Availability: Proximity of the necessary infrastructure required for access. Affordability: The cost of access relative to income. Relevance: A reason for access, such as primary language content. Readiness: The capacity to access, including skills, awareness and cultural acceptance.

The number of LTE users crossed 1 Billion, end of 2015 according to a report by GSA. OpenSignal has a summary blog post on this here.

Finally, Open Signal has published Global State of LTE Market report that provides coverage, speeds and a lot more information.

South Korea and Singapore have set themselves apart from the main body of global operators, providing both superior coverage and speed. The biggest standouts were South Korea’s Olleh and Singapore’s Singtel. Olleh excelled in coverage, but also provided one of the fastest connections speeds in our report, 34 Mbps. Meanwhile Singtel hit the 40 Mbps mark in speed while still maintaining a coverage rating of 86%. There are other notable country clusters in the upper right-hand quadrant as well, for instance operators from the Netherlands, Canada and Hungary. Meanwhile, other countries have staked positions for themselves in specific regions of the plot. U.S. and Kuwaiti operators are tightly clustered in the lower right, meaning they offer excellent coverage but poor 4G speeds. Japan and Taiwan congregate in the middle far right with their exceptional coverage but only average speeds. Most of New Zealand and Romania’s operators hover at the center top of the chart, indicating impressive bandwidth but a general lack of availability.

Its makes interesting reading, PDF available here.

*** Added Later: 25/03/16:12.15 ***

A good breakdown of LTE subscriptions by countries by Ovum:

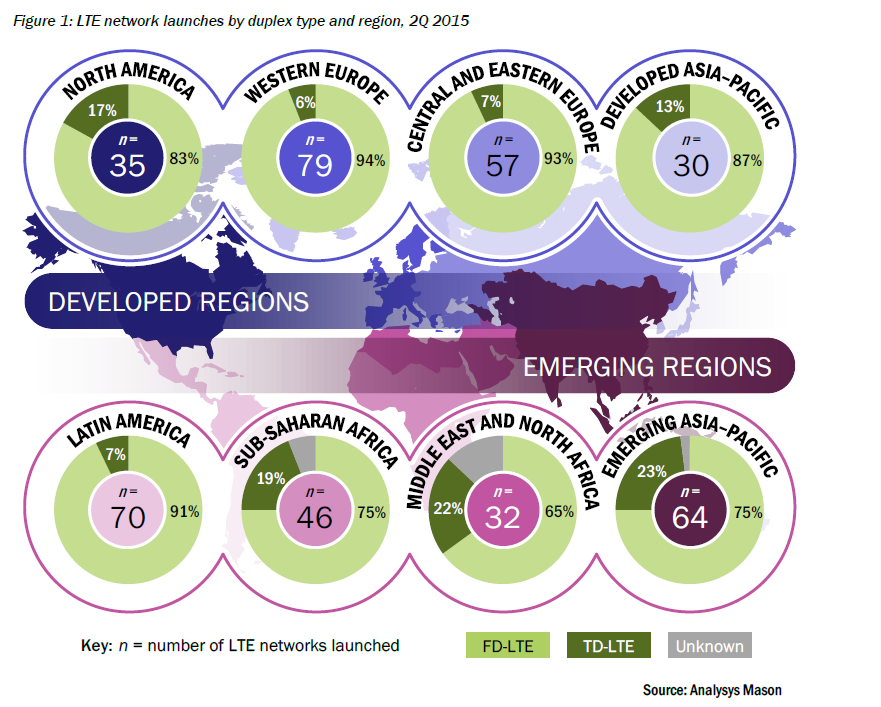

As per Analysis Mason, of the 413 commercial LTE networks that have been launched worldwide by the end of 2Q 2015, FD-LTE accounts for 348 (or 84%) of them, while TD-LTE accounts for only 55 (or 13%). Having said that, TD-LTE will be growing in market share, thanks to the unpaired spectrum that many operators secured during the auctions. This, combined with LTE-A Small Cells (as recently demoed by Nokia Networks) can help offload traffic from hotspots.

China Mobile has managed to sign up more than 200 million subscribers in just 19 months, making it the fastest-growing operator in the world today. It has now deployed 900,000 basestations in more than 300 cities. From next year, it is also planning to upgrade to TDD+ which combines carrier aggregation and MIMO to deliver download speeds of up to 5 Gbit/s and a fivefold improvement in spectrum efficiency. TDD+ will be commercially available next year and while it is not an industry standard executives say several elements have been accepted by 3GPP.

SoftBank Japan has revealed plans to trial LTE-TDD Massive MIMO, a likely 5G technology as well as an important 4G enhancement, from the end of the year. Even though it was one of the world's first operators to go live with LTE-TDD, it has until now focused mainly on its LTE-FDD network. It has rolled out 70,000 FDD basestations, compared with 50,000 TDD units. But TDD is playing a sharply increasing role. The operator expects to add another 10,000 TDD basestations this year to deliver additional capacity to Japan's data-hungry consumers. By 2019 at least half of SoftBank's traffic to run over the TDD network.

According to the Analysis Mason article, Operators consider TD-LTE to be an attractive BWA (broadband wireless access) replacement for WiMAX because:

most WiMAX deployments use unpaired, TD spectrum in the 2.5GHz and3.5GHz bands, and these bands have since been designated by the 3GPP as being suitable for TD-LTE

TD-LTE is 'future-proof' – it has a reasonably long evolution roadmap and should remain a relevant and supported technology throughout the next decade

TD-LTE enables operators to reserve paired FD spectrum for mobile services, which mitigates against congestion in the spectrum from fixed–mobile substitution usage profiles.

For people who may be interested in looking further into migrating from WiMAX to TD-LTE, may want to read this case study here.

I have looked at the joint FDD-TDD CA earlier here. The following is from the 4G Americas whitepaper on Carrier Aggregation embedded here.

Previously, CA has been possible only between FDD and FDD spectrum or between TDD and TDD spectrum. 3GPP has finalized the work on TDD-FDD CA, which offers the possibility to aggregate FDD and TDD carriers jointly. The main target with introducing the support for TDD-FDD CA is to allow the network to boost the user throughput by aggregating both TDD and FDD toward the same UE. This will allow the network to boost the UE throughput independently from where the UE is in the cell (at least for DL CA). TDD and FDD CA would also allow dividing the load more quickly between the TDD and FDD frequencies. In short, TDD-FDD CA extends CA to be applicable also in cases where an operator has spectrum allocation in both TDD and FDD bands. The typical benefits of CA – more flexible and efficient utilization of spectrum resources – are also made available for a combination of TDD and FDD spectrum resources. The Rel-12 TDD-FDD CA design supports either a TDD or FDD cell as the primary cell. There are several different target scenarios in 3GPP for TDD-FDD CA, but there are two main scenarios that 3GPP aims to support. The first scenario assumes that the TDD-FDD CA is done from the same physical site that is typically a macro eNB. In the second scenario, the macro eNB provides either a TDD and FDD frequency, and the other frequency is provided from a Remote Radio Head (RRH) deployed at another physical location. The typical use case for the second scenario is that the macro eNB provides the FDD frequency and the TDD frequency from the RRH.

Nokia Networks were the first in the world with TDD-FDD CA demo, back in Feb 2014. In fact they also have a nice video here. Surprisingly there wasnt much news since then. Recently Ericsson announced the first commercial implementation of FDD/TDD carrier aggregation (CA) on Vodafone’s network in Portugal. Vodafone’s current trial in its Portuguese network uses 15 MHz of band 3 (FDD 1800) and 20 MHz of band 38 (TDD 2600). Qualcomm’s Snapdragon 810 SoC was used for measurement and testing.

3 Hong Kong is another operator that has revealed its plans to launch FDD-TDD LTE-Advanced in early 2016 after demonstrating the technology on its live network. The operator used equipment supplied by Huawei to aggregate an FDD carrier in either of the 1800 MHz or 2.6 GHz bands with a TDD carrier in the 2.3 GHz band. 3 Hong Kong also used terminals equipped with Qualcomm's Snapdragon X12 LTE processor. 3 Hong Kong already offers FDD LTE-A using its 1800-MHz and 2.6-GHz spectrum, and is in the midst of deploying TD-LTE with a view to launching later this year. The company said it expects devices that can support hybrid FDD-TDD LTE-A to be available early next year "and 3 Hong Kong is expected to launch the respective network around that time." 3 Hong Kong also revealed it plans to commercially launch tri-carrier LTE-A in the second half of 2016, and is working to aggregate no fewer than five carriers by refarming its 900-MHz and 2.1-GHz spectrum.

TDD-FDD CA is another tool in the network operators toolbox to help plan the network and make it better. Lets hope more operators take the opportunity to deploy one.

People often ask at various conferences if TD-LTE is a fad or is it something that will continue to exist along with the FDD networks. TDD networks were a bit tricky to implement in the past due to the necessity for the whole network to be time synchronised to make sure there is no interference. Also, if there was another TDD network in an adjacent band, it would have to be time synchronised with the first network too. In the areas bordering another country where they might have had their own TDD network in this band, it would have to be time synchronised too. This complexity meant that most networks were happy to live with FDD networks.

In 5G networks, at higher frequencies it would also make much more sense to use TDD to estimate the channel accurately. This is because the same channel would be used in downlink and uplink so the downlink channel can be estimated accurately based on the uplink channel condition. Due to small transmit time intervals (TTI's), these channel condition estimation would be quite good. Another advantage of this is that the beam could be formed and directed exactly at the user and it would appear as a null to other users.

This is where 8T8R or 8 Transmit and 8 Receive antennas in the base station can help. The more the antennas, the better and narrower the beam they can create. This can help send more energy to users at the cell edge and hence provide better and more reliable coverage there.

How do these antennas look like? 8T8R needs 8x Antennas at the Base Station Cell, and this is typically delivered using four X-Polar columns about half wavelength apart. I found the above picture on antenna specialist Quintel's page here, where the four column example is shown right. At spectrum bands such as 2.3GHz, 2.6GHz and 3.5GHz where TD-LTE networks are currently deployed, the antenna width is still practical. Quintel’s webpage also indicates how their technology allows 8T8R to be effectively emulated using only two X-Polar columns thus promising Slimline antenna solutions at lower frequency bands. China Mobile and Huawei have claimed to be the first ones to deploy these four X-Pol column 8T8R antennas. Sprint, USA is another network that has been actively deploying these 8T8R antennas.

There are couple of interesting tweets that show their kit below:

Sprint's John Saw showing of TD-LTE 8T8R and Network Vision. Room for expansion. pic.twitter.com/Mydzasg3F6

Sprint's deployment of 8T8R (eight-branch transmit and eight-branch receive) radios in its 2.5 GHz TDD LTE spectrum is resulting in increased data throughput as well as coverage according to a new report from Signals Research. "Thanks to TM8 [transmission mode 8] and 8T8R, we observed meaningful increases in coverage and spectral efficiency, not to mention overall device throughput," Signals said in its executive summary of the report. The firm said it extensively tested Sprint's network in the Chicago market using Band 41 (2.5 GHz) and Band 25 (1.9 GHz) in April using Accuver's drive test tools and two Galaxy Note Edge smartphones. Signals tested TM8 vs. non-TM8 performance, Band 41 and Band 25 coverage and performance as well as 8T8R receive vs. 2T2R coverage/performance and stand-alone carrier aggregation. Sprint has been deploying 8T8R radios in its 2.5 GHz footprint, which the company has said will allow its cell sites to send multiple data streams, achieve better signal strength and increase data throughput and coverage without requiring more bandwidth. The company also has said it will use carrier aggregation technology to combine TD-LTE and FDD-LTE transmission across all of its spectrum bands. In its fourth quarter 2014 earnings call with investors in February, Sprint CEO Marcelo Claure said implementing carrier aggregation across all Sprint spectrum bands means Sprint eventually will be able to deploy 1900 MHz FDD-LTE for uplink and 2.5 GHz TD-LTE for downlink, and ultimately improve the coverage of 2.5 GHz LTE to levels that its 1900 MHz spectrum currently achieves. Carrier aggregation, which is the most well-known and widely used technique of the LTE Advanced standard, bonds together disparate bands of spectrum to create wider channels and produce more capacity and faster speeds.

Alcatel-Lucent has a good article in their TECHzine, an extract from that below:

Field tests on base stations equipped with beamforming and 8T8R technologies confirm the sustainability of the solution. Operators can make the most of transmission (Tx) and receiving (Rx) diversity by adding in Tx and Rx paths at the eNodeB level, and beamforming delivers a direct impact on uplink and downlink performance at the cell edge. By using 8 receiver paths instead of 2, cell range is increased by a factor of 1.5 – and this difference is emphasized by the fact that the number of sites needed is reduced by nearly 50 per cent. Furthermore, using the beamforming approach in transmission mode generates a specific beam per user which improves the quality of the signal received by the end-user’s device, or user equipment (UE). In fact, steering the radiated energy in a specific direction can reduce interference and improves the radio link, helping enable a better throughput. The orientation of the beam is decided by shifting the phases of the Tx paths based on signal feedback from the UE. This approach can deliver double the cell edge downlink throughput and can increase global average throughput by 65 per cent. These types of deployments are made possible by using innovative radio heads and antenna solutions. In traditional deployments, it would require the installation of multiple remote radio heads (RRH) and multiple antennas at the site to reach the same level of performance. The use of an 8T8R RRH and a smart antenna array, comprising 4 cross-polar antennas in a radome, means an 8T8R sector deployment can be done within the same footprint as traditional systems.

Anyone interested in seeing pictures of different 8T8R antennas like the one above, see here. While this page shows Samsung's antennas, you can navigate to equipment from other vendors.

Finally, if you can provide any additional info or feel there is something incorrect, please feel free to let me know via comments below.

Ericsson mobility report 2015 was released last week. Its interesting to see quite a few of these stats on devices, traffic, usage, etc. is getting released around this time. All of these reports are full of useful information and in the old days when I used to work as an analyst, I would spend hours trying to dig into them to find gold. Anyway, some interesting things as follows and report at the end.

The above chart, as expected, data will keep growing but voice will get flatter and maybe go down, if people start moving to VoIP

Interesting chart showing the breakdown of usage from heavy mobile data users to light mobile data users. pic.twitter.com/ew2Z0rWzlZ

Application volume shares, based on the data plan. This is interesting. If you are a heavy user, you may be watching a lot of videos and if you are a light user then you are watching just a few of them.

Good chart looking at how device screen size impacts certain mobile tasks more than others. Video mainly. pic.twitter.com/DcuS1rJway